Financial Accounting Framework

In March 2012 the XRB Board issued a document outlining a new Accounting Standards Framework that will become effective progressively over the period 2012-2016. That document, which was entitled "Proposals for the New Zealand Accounting Standards Framework Incorporating the Draft Tier Strategy", and which was approved by the Minister of Commerce in April 2012, is available here.

The Accounting Standards Framework was updated in December 2015 to reflect legislative changes since 2012 and the manner in which the Tier requirements are described. The updated Accounting Standards Framework is available here.

The finalisation of the new Accounting Standards Framework followed a development and consultation process that occurred over the four-year period from 2008 – 2012. Further information about the process, and the matters considered as part of the development of the new Accounting Standards Framework, is available here.

Overview of Accounting Standards Framework

The new Accounting Standards Framework involves a two sector, multi-standards, tiered approach as summarised in the following table. For further details please see the Accounting Standards Framework document.

| For-Profit Entities

|

Public Benefit Entities

|

|||

|---|---|---|---|---|

| Entities | Accounting Standards

|

Entities

|

Accounting Standards

|

|

| Tier 1

|

Publicly accountable (as defined); or

Large (as defined) for-profit public sector entities |

NZ IFRS

|

Publicly accountable (as defined); or Large (as defined)

|

PBE Standards

|

| Tier 2 | Non-publicly accountable and

Non-large for-profit public sector entities Which elect to be in Tier 2. |

NZ IFRS Reduced Disclosure Regime

(NZ IFRS RDR) |

Non-publicly accountable (as defined) and non-large (as defined)

Which elect to be in Tier 2 |

PBE Standards Reduced Disclosure Regime (PBE Standards RDR)

|

| Tier 3

|

Non-publicly accountable and either all of its owners are members of the entity's governing body; or not large (as defined)

Which elect to be in Tier 3* |

NZ IFRS Differential Reporting (NZIFRS Diff Rep)*

|

Non-publicly accountable (as defined) with expenses ≤ 2 million

which elect to be in Tier 3. |

PBE Simple Format Reporting Standard - Accrual (PSFR-A) |

| Tier 4

|

Non-publicly accountable, not required to file financial statements, and not large (as defined)

which elect to be in Tier 4.* |

Old GAAP* | Entities allowed by law to use cash accounting

which elect to be in Tier 4. |

PBE Simple Format Reporting Standard - Cash (PSFR-C)

|

*Transitional tier which will be removed when legislative changes come into force.

The criteria for, and reporting requirements for, For-Profit Tiers 3 and 4 reflect the status quo for entities currently using NZ IFRS differential reporting or Old GAAP (SSAPs and FRSs). These are transitional tiers which will be removed when legislative changes provided for in the Financial Reporting Bill 2012 come into force. Those legislative changes will remove the statutory requirement from most small and medium sized companies to prepare financial statements in accordance with GAAP.

Policy Approach to Developing PBE Standards

In September 2013 the XRB issued a policy paper entitled “Policy Approach to Developing PBE Standards”. Although published separately, the Policy Approach can be thought of as equivalent to an addendum to the Accounting Standards Framework document. It is designed to elaborate on the approach outlined in paragraphs 149-151 of that document.

The Policy Approach paper establishes an approach, based on a “development principle” and a series of “rebuttable presumptions”, which will be used by the NZASB to determine whether, and when, to make changes to the suite of PBE Standards.

Roll-out of the New Accounting Standards Framework

The implementation of the Accounting Standards Framework requires the development and issuing of several new suites of accounting standards. The XRB Board plans to issue exposure drafts and then finalise and issue the suites of standards in a five stage process. Different release and submission dates will apply to each stage.

YOU MIGHT ALSO LIKE

Share this Post

Related posts

Financial Accounting Careers

As a financial accountant, you may choose to work in public accounting (doing jobs for multiple business clients) or private…

Read More

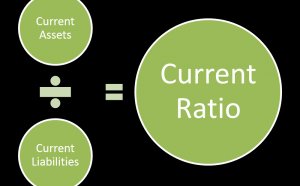

Financial Accounting current ratio

The current ratio is a financial ratio that shows the proportion of current assets to current liabilities. The current ratio…

Read Morelatest post

-

Relevance in Financial Accounting November 29, 2017

Relevance in Financial Accounting November 29, 2017 -

Financial Accounting Careers November 26, 2017

Financial Accounting Careers November 26, 2017 -

Financial Accounting Standard Setting in the United State November 23, 2017

Financial Accounting Standard Setting in the United State November 23, 2017 -

Dell Financial account November 20, 2017

Dell Financial account November 20, 2017 -

LPL Financial my account November 17, 2017

LPL Financial my account November 17, 2017 -

Learn Financial Accounting November 14, 2017

Learn Financial Accounting November 14, 2017 -

Financial statements definition in Accounting November 11, 2017

Financial statements definition in Accounting November 11, 2017 -

Financial Accounting for non Profit Organizations November 8, 2017

Financial Accounting for non Profit Organizations November 8, 2017 -

Financial Accounting Programs November 5, 2017

Financial Accounting Programs November 5, 2017