Financial Accounting Standards

Share this Post

Related posts

Financial Accounting Standards Board History

JULY 06, 2026

Since 1973, the Financial Accounting Standards Board (FASB) has been the designated organisation in the private sector for…

Read More

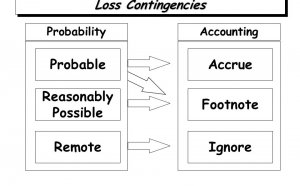

Financial Accounting Standards No. 5

JULY 06, 2026

Presentation Chapter 13-1 Current Liabilities and Contingencies

Read Morelatest post

-

Relevance in Financial Accounting November 29, 2017

Relevance in Financial Accounting November 29, 2017 -

Financial Accounting Careers November 26, 2017

Financial Accounting Careers November 26, 2017 -

Financial Accounting Standard Setting in the United State November 23, 2017

Financial Accounting Standard Setting in the United State November 23, 2017 -

Dell Financial account November 20, 2017

Dell Financial account November 20, 2017 -

LPL Financial my account November 17, 2017

LPL Financial my account November 17, 2017 -

Learn Financial Accounting November 14, 2017

Learn Financial Accounting November 14, 2017 -

Financial statements definition in Accounting November 11, 2017

Financial statements definition in Accounting November 11, 2017 -

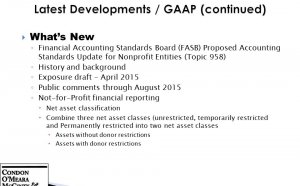

Financial Accounting for non Profit Organizations November 8, 2017

Financial Accounting for non Profit Organizations November 8, 2017 -

Financial Accounting Programs November 5, 2017

Financial Accounting Programs November 5, 2017